There are a some steps the user should perform for each SCR calculation workbook, to bring in external (EIOPA or BoE) reference data for the calculation reference date:

1. Import the risk-free rate

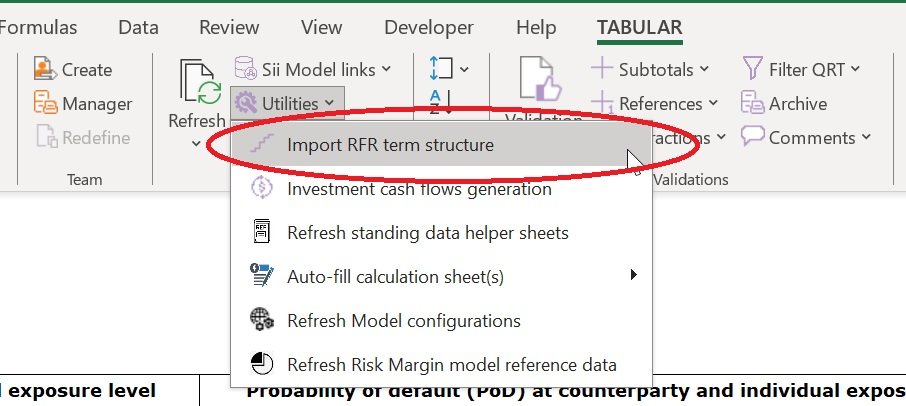

STEP 1 – Open the import window from Sii Model > Utilities > Import RFR term structure:

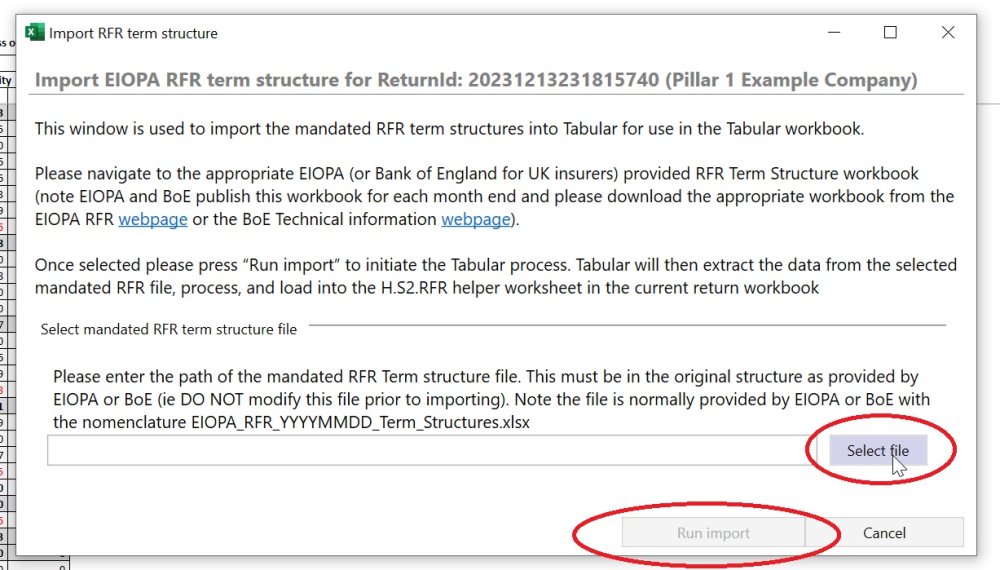

STEP 2 – From this screen you should navigate to the EIOPA or Bank of England published Excel file (these files should be downloaded outside of Tabular from the EIOPA or BoE webpage beforehand. There are links to these pages within the Tabular window) containing the risk-free interest rate term structures information, using “Select file” and once selected click “Run import”:

2. Enter the symmetric equity adjustment

Note if there are no exposures that fall within the Market module > Equity sub-module, then this step is not required.

Go to sheet H.Configs.Input and enter the symmetric adjustment amount (as a ratio) in the row where [Configuration] is “EquitySymmetricAdj”. For example in the below screen the symmetric adjustment is -1.7895997%

Post your comment on this topic.