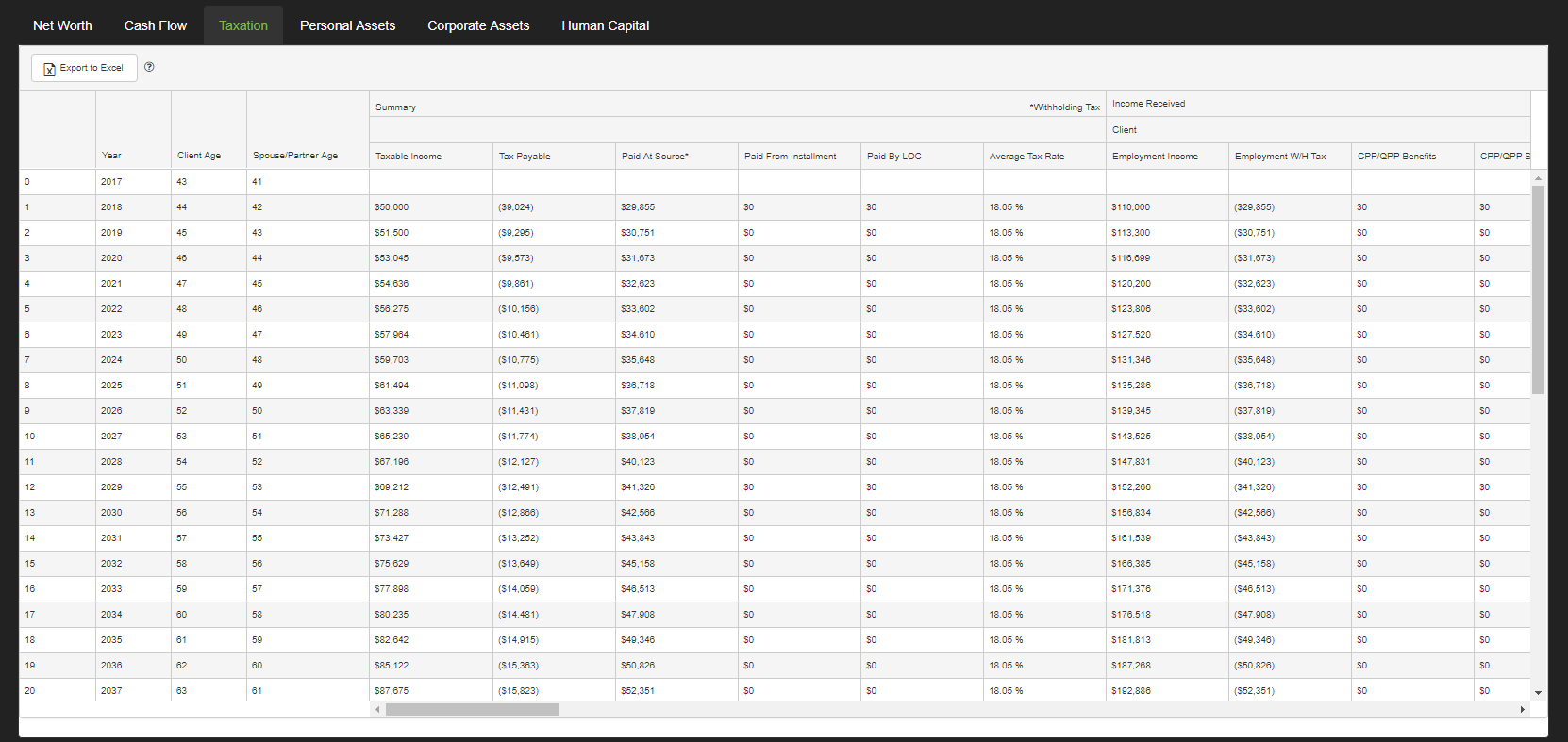

The Taxation ledger tab outlines the income and tax calculations for each year of the analysis.

Summary

- Taxable Income – The sum of client and spouse/partner taxable income.

- Tax Payable – The sum of client and spouse/partner tax payable.

- Paid At Source – The total annual tax withheld at source. Withholding tax is calculated on income from Retirement Investments (above the minimums), Pension Plans and OAS.

- Paid By Instalment – The total annual taxes paid on investment withdrawals.

- Paid By LOC – The total annual taxes paid by the Lifestyle Line of Credit. When the tax payable is greater than the amount paid at source or by installment, the Lifestyle Line of Credit is used to pay the taxes and help offset any possible shortfall.

- Average Tax Rate – The combined average tax rate of the client and spouse/partner calculated as Tax Payable divided by Taxable Income.

Income Received – Client and Spouse/Partner

- Employment Income – The before tax annual income from employment. The amount displayed is the sum of data entered in employment income from both Step 1 and Step 2 of data entry.

- Employment W/H Tax – Taxes withheld at source on employment income.

- CPP/QPP Benefits – The annual benefits from CPP/QPP, amount is displayed prior to withholding taxes and any income splitting.

- CPP/QPP Split – Portion of the CPP/QPP that is being split with a spouse or received from a spouse. Negative values indicate a reduction in CPP income being received, positive values indicate an increase in CPP income.

- OAS Benefits – The annual benefits from Old Age Security prior to withholding taxes and claw-back.

- OAS Claw-Back – When a client is receiving Old Age Security income but their income is above a threshold, the age credit is clawed back through the use of a recovery tax.

- Pension Income – Annual income from a Defined Benefit pension plan.

- Pension Split (Net) – Portion of pension income being split with a spouse for income tax purposes. Positive values indicate that pension income is being added while negative values indicate that pension income is being subtracted.

- Pension W/H Tax – Withholding taxes that are payable on any pension income received.

- Other Income – Annual income received from other sources, this amount comes from the data entered in other income in both Step 1 and Step 2 of data entry.

- Tax-Free Portion – A percentage of the amounts entered into Other Income can be designated as tax-free, this amount represents the tax free portion of the other income. This value is displayed as a negative value as it is used to reduce the taxable income.

- Registered Withdrawals – The portion of the total income/withdrawals from registered plans including RRSP, RRIF, and Locked-In Plans that is received.

- Registered W/H Tax – Withholding taxes that are payable on the registered withdrawals received.

- Dividends – The annual total dividends that are paid from the corporate investment account.

- Dividend Gross-up – The amount the corporate investment dividends are grossed up for tax purposes. This amount will be added to the value in the Corporate Investments column when calculating taxable income.

- Investment Income – The annual income received from the Non-Registered accounts.

- Tax Deductions – Annual tax deduction created from contributions to RRSP and Locked-In Retirement Accounts.

Income Tax – Client and Spouse/Partner

- Taxable Income – The taxable portion of income for each client. This is the total income minus any non-taxable investment growth (Tax Efficiency) and deductions.

- Basic Tax Payable – The amount of tax payable before credits, based on Taxable Income. RazorPlan uses federal and provincial tax brackets to arrive at this amount.

- Age Credit – The age tax credit amount received each year. Applicable to clients when 65 or older.

- Pension Credit – The pension credit each year by clients who receive pension income.

- Age Credit Recovery Tax – When a client is receiving the age credit but their income is above a threshold, the age credit is clawed back through the use of a recovery tax. See the Effective Tax Rate calculation for more information.

- OAS Recovery Tax – When a client is receiving Old Age Security income but their income is above a threshold, their OAS income benefit is clawed back through the use of a recovery tax. See the Effective Tax Rate calculation for more information.

- CPP/EI Deductions – Annual amount being deducted from employment income for the CPP contributions and EI payments.

- Net Tax Payable – Calculated as Basic Tax Payable – Age Credit – Pension Credit + Age Credit Recovery Tax + OAS Recovery Tax + CPP/EI Deductions.

- Marginal Tax Rate – The rate of tax applied to the last dollar of taxable income earned. The rate is comprised of the combined federal and provincial rates.

- Clawback Rate – The rate of recovery tax used to clawback the age credit and/or Old Age Security.

- Effective Tax Rate – Represents the highest tax paid on any one dollar of taxable income when including the Clawback Rate. See the Effective Tax Rate calculation for more information.

- Average Tax Rate – Calculated as Net Tax Payable divided by Taxable Income. This amount represents the percentage of tax that is paid on average.

Need more help with this?

Contact Razor Support