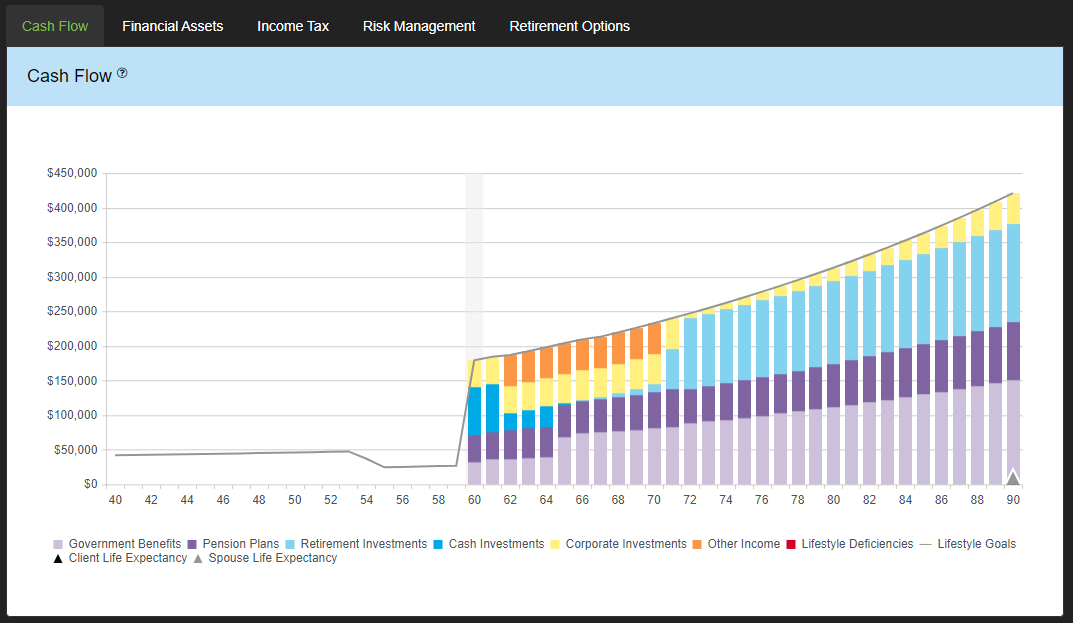

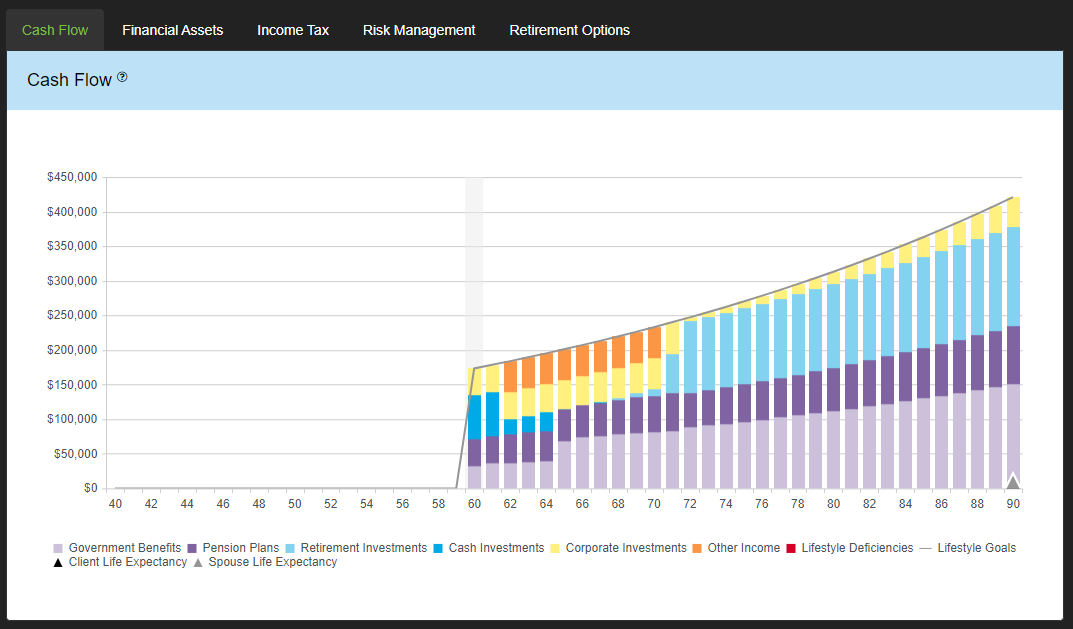

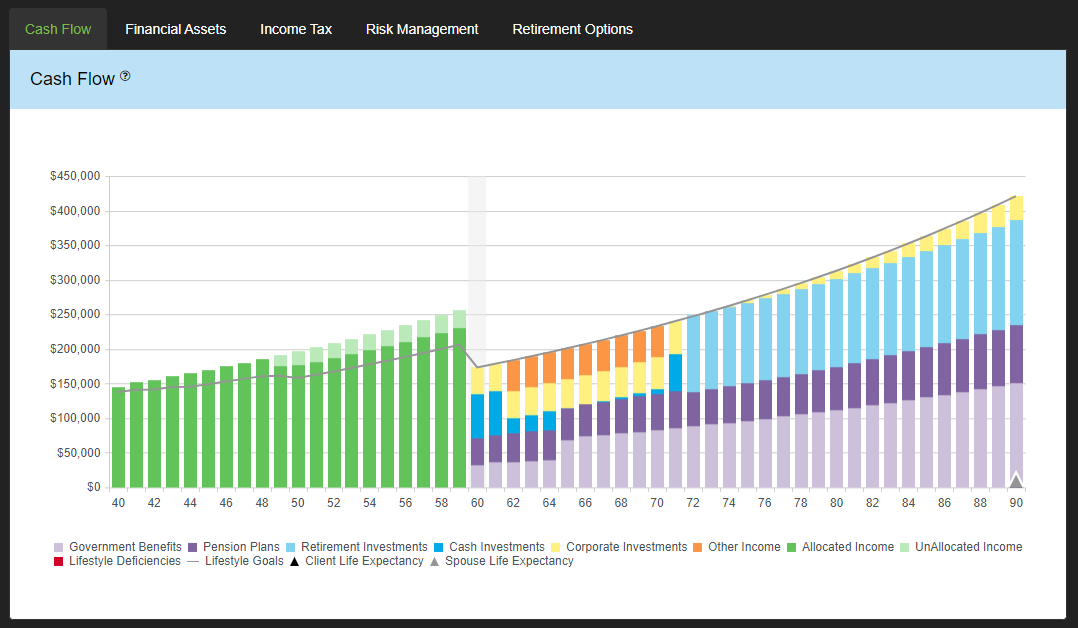

The Cash Flow chart allows you to see whether a client will or will not run out of liquid assets at some point in the future. The Cash Flow chart has two states depending on the Pre-Retirement Cash Flow setting in Your Account. As indicated by the name this setting will impact how the cash flow chart displays in the pre-retirement years, post retirement years will display the same in both states.

When pre-retirement cash flow is set to Off, the Cash Flow chart ignores pre-retirement lifestyle expenditures and shows only planned savings, debt payments and capital needs (if applicable) as the pre-retirement lifestyle goals.

When pre-retirement cash flow is set to On, the Cash Flow chart displays pre-retirement income and indicates if the income is allocated or unallocated. In this state you can use the Excess Cash Flow feature to manage the unallocated income.

Cash Flow Breakdown

- Government Benefits – The combined value of both Client and Spouse CPP/QPP and OAS.

- Pension Plans – The combined value of both Client and Spouse pensions. Pension income will be indexed to inflation pre-retirement, and the pension indexing assumption post-retirement.

- Retirement Investments – The combined value of Client and Spouse RRSP/RRIF and Locked-In Plan withdrawals.

- Cash Investments – The combined value of Client, Spouse, and Joint Non-Registered and TFSA Investment withdrawals.

- Corporate Investments – Total Corporate Investment withdrawals, this includes both RDTOH (refundable dividend tax on hand) and dividends used to fill Retirement Income Needs.

- Other Income – The combined value of all other fixed income sources other than CPP/QPP, OAS and Pensions.

- Allocated Income – The combined value of Client and Spouse incomes from employment and other sources that are allocated towards lifestyle, investment savings and debt payments.

- Unallocated Income – The combined value of Client and Spouse incomes from employment and other sources that have not yet been allocated towards lifestyle, investment savings and debt payments.

- Lifestyle Deficiencies – Lifestyle deficiencies are shortfalls in cash flow that occur when lifestyle goals are greater than all sources of income, these amounts are automatically added to the Lifestyle Line of Credit.

- Lifestyle Goals – In pre-retirement years the lifestyle goals will display the planned expenditure, when pre-retirement cash flow is turned on, plus planned savings and debt payments. In retirement this line is the planned expenditures and RazorPlan will look to fund this goal with the income and assets available.

- Client Life Expectancy – The client’s assumed life expectancy that has been entered.

- Spouse Life Expectancy – The spouse’s assumed life expectancy that has been entered. This indicator will be displayed at the client’s age that is equal to the year the spouse’s assumed life expectancy is reached.

Need more help with this?

Contact Razor Support