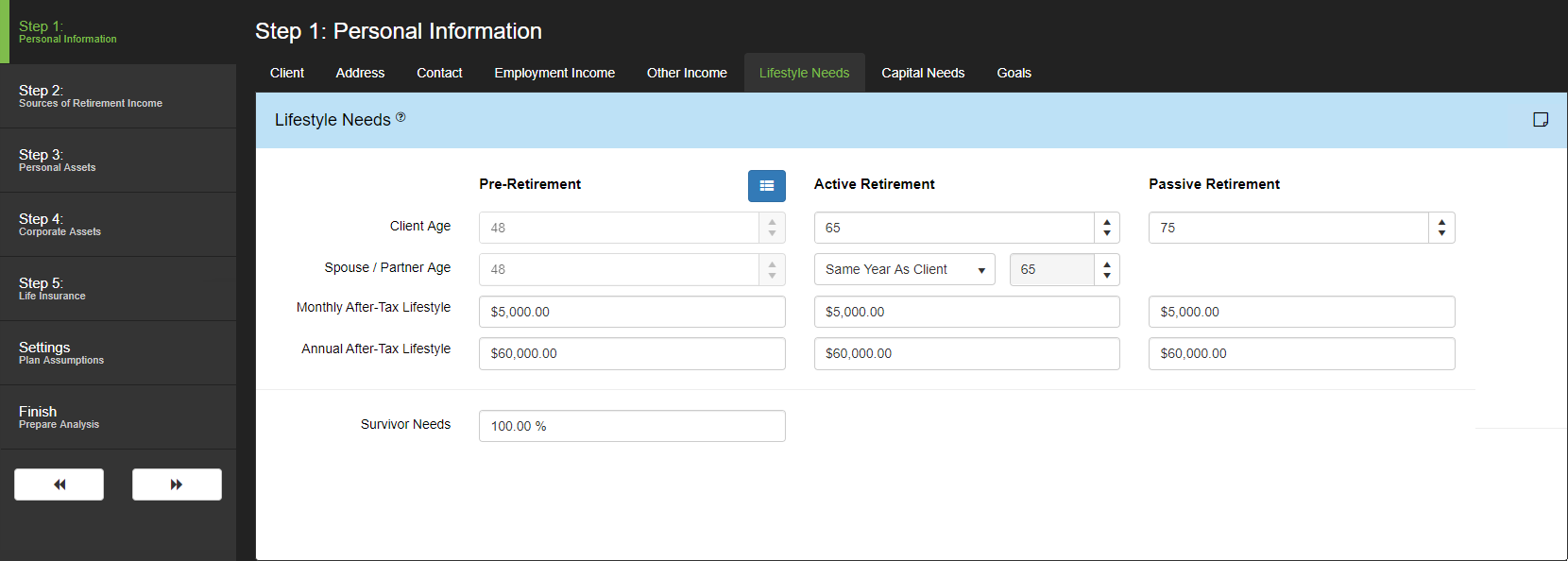

There are 3 possible lifestyle stages available; Pre-Retirement, Active Retirement and Passive Retirement. The Pre-Retirement state will end when the Active Retirement stage begins and the Active Retirement stage will automatically end when Passive Retirement stage begins; this final stage ends at life expectancy.

The Lifestyle Needs data entry screen displays different fields depending on the Pre-Retirement Cash Flow setting on the Assumptions tab of Your Account. If Pre-Retirement Cash Flow is on this screen will display fields for Pre-Retirement lifestyle needs and hides the Add Debt Payments, Add Investment Savings and Add Insurance Premiums fields.

When the Pre-Retirement Cash Flow setting in Assumptions set to Off, the Lifestyle Needs data entry screen will display the Add Debt Payments, Add Investment Savings and Add Insurance Premiums fields while hiding the Monthly and Annual Income fields under the Pre-Retirement stage.

Client Age: Set the ages at which the Client retires and will begin Active Retirement. Passive Retirement age is used to indicate an age after retirement when lifestyle changes. Pre-retirement age fields will always equal the current age of the client.

Spouse/Partner Age: When building a Joint plan, the Spouse/Partner Active Retirement can be set independently of the Client. Select ‘Same Year as Client’ from the drop-down to indicate that the Client and Spouse/Partner will retire at the same time, or select ‘At Age’ to establish a separate retirement age for the Spouse/Partner. Passive Retirement for the Spouse/Partner will always start at the same time as Client.

Monthly After-Tax Income: Enter the after-tax monthly income needs in today’s dollars and the Annual After-Tax Income field will automatically update. This value will grow with inflation. If no value is entered, RazorPlan will auto-calculate a monthly income need when the analysis is calculated.

Annual After-Tax Income: Enter the after-tax annual income needs in today’s dollars and the Monthly After-Tax Income field will automatically update. This value will grow with inflation. If no value is entered, RazorPlan will auto-calculate an annual income need when the analysis is calculated.

Survivor Needs: Enter the percentage the lifestyle need will be reduced to when either the client or spouse/partner becomes a survivor of the other. The age this reduced lifestyle starts is controlled by life expectancy. This field is only visible when Assumed Life Expectancy is selected in Assumptions.

Add Debt Payments: To include any mortgage debts in the clients’ lifestyle, select ‘Yes’ from the drop down. This will automatically add any remaining mortgage payments, entered under Real Estate, to the clients’ lifestyle needs. Once the mortgage balance is paid off, the lifestyle need will reduce accordingly.

Add Investment Savings: To include any planned investment savings (RRSPs, LIRAs, TFSAs and Non-registered) in the clients’ lifestyle, select ‘Yes’ from the drop down. This selection automatically adds any planned deposits entered under Step 3: Personal Assets, to the clients’ lifestyle needs enter on this screen.

Add Ins. Premiums: To include any life insurance premiums in the clients’ lifestyle, select ‘Yes’ from the drop down. This selection will automatically add the insurance premiums, entered under Life Insurance, to the clients’ lifestyle needs. Any increases or decreases in these premiums will automatically be reflected in the lifestyle needs. (Only available in RazorPlan Advanced. You can upgrade to RazorPlan Advanced using the Billing tab in Your Account. If you have any questions, please contact support).

*In some cases, it is possible that clients could have a one-time lump sum or periodic recurring expense. In this situation, it is recommended you enter the extra need through the Retirement Needs Drill-Down  .

.

Need more help with this?

Contact Razor Support