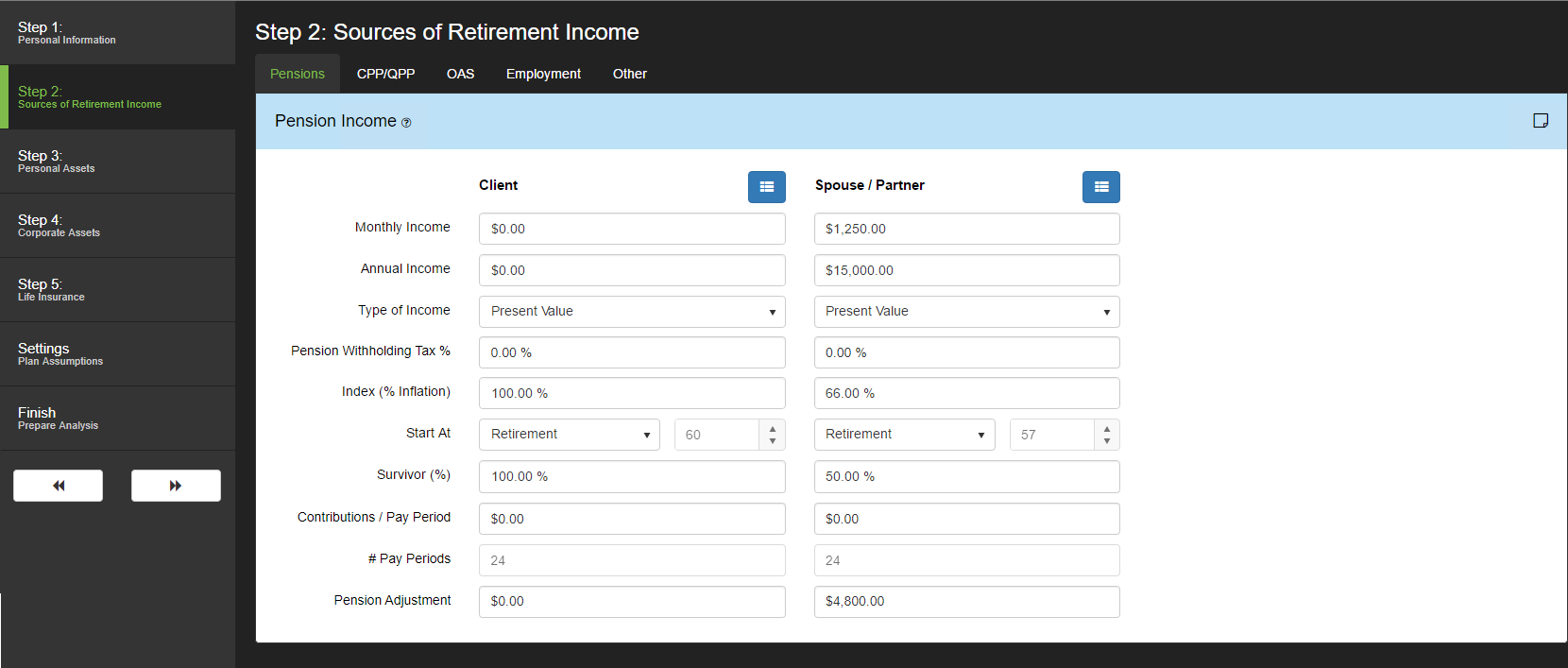

If your client is expecting to receive retirement income from a Defined Benefit pension, enter the expected income as a pre-tax monthly or annual amount (in today’s dollars). If they are currently retired, enter the amount they are receiving today.

*In some cases, it is possible that a client could also be receiving income from more than one pension plan and/or a bridge benefit. In this situation it is recommended you enter the extra income through the Pension Drill-Down  .

.

Monthly Income: Enter the expected monthly taxable pension income. The software will automatically calculate the annual income expected based on the monthly income entered. Enter any Defined Contribution pensions in the Locked-In Plans section.

Annual Income: Enter the expected annual taxable pension income. The software will automatically calculate the monthly income expected based on the annual income entered. Enter any Defined Contribution pensions in the Locked-In Plans section.

Type of Income: Pension Income can be entered in either today’s dollars or in future dollars. Based on the method you choose, select either Present Value or Future Value from the drop down.

Pension Withholding Tax % Enter the percentage of pension income that is withheld at source for taxes. The amount entered into this field will impact the pension income received for cash flow planning in retirement.

Index (% inflation): If the pension income offers indexing, enter the expected indexing as a percent of inflation. For example, if inflation is entered at 3% and you enter 50% in this field, the software will assume an increase of 1.5% per year once income begins. Prior to retirement, the software will index the expected pension income at 100% of inflation.

Start At: Select ‘Retirement’ from the drop-down to have the pension income begin at retirement, or select ‘Age’ to establish a specific age.

Survivor (%): Some pensions offer a survivor benefit allowing a portion of the income to pass on to a surviving spouse should a client die. Enter the survivor portion as a percent of the total income. Although the software will never show the death of a client, the software requires this information to properly calculate a client’s Human Capital value.

Contribution / Pay Period Enter the amount of contributions to the pension plan that the clients are making based on the number of pay periods entered below. This amount is multiplied by the number of pay periods to create a tax deduction in the tax calculations.

Number Pay Periods Enter the number of pay periods per year for the pension contributions. For clients that are paid bi-weekly they would have 26 pay periods whereas clients that are paid semi-monthly have 24 pay periods per year.

Pension Adjustment: In situations where a client is part of a Defined Benefit Pension, enter the Pension Adjustment listed on the client’s previous year’s Notice of Assessment. This value will offset the available Contribution Limit and will impact the ability to enter future RRSP contributions. RazorPlan will not allow RRSP contributions beyond the available limit. In situations where a client is part of a Defined Contribution Pension, the software will automatically reduce the available contribution room by the contributions entered, no Pension Adjustment is required.

Need more help with this?

Contact Razor Support