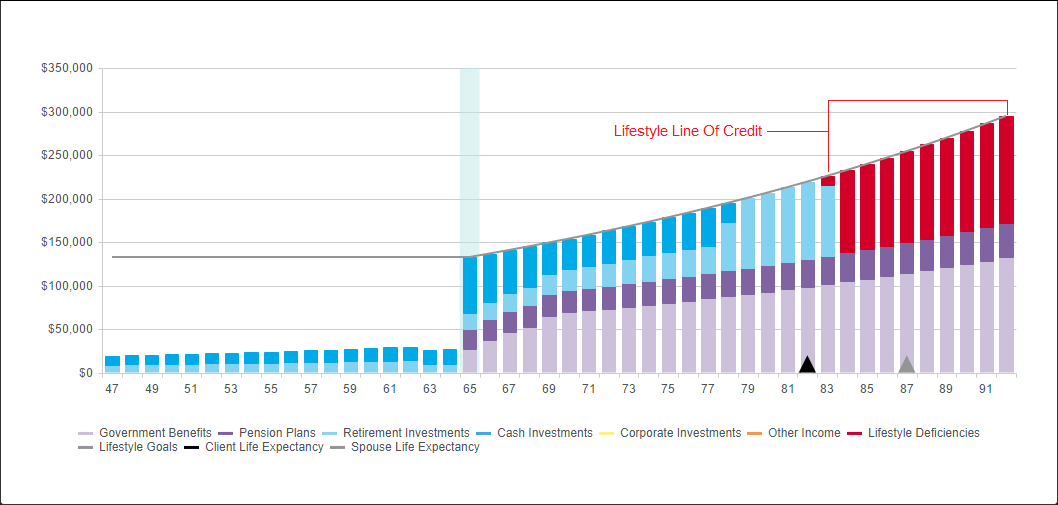

When a client is short of funding their retirement goals, the software will attempt to fill these deficiencies through the use of Lifestyle Line of Credit. By offsetting deficiencies through the use of debt, you can determine whether there are sufficient fixed assets available to fund Retirement Income Needs.

The software will borrow against the client’s Lifestyle Line of Credit in years where there are insufficient liquid assets and fixed income to meet their goals. This approach will maintain the client’s lifestyle while accumulating Lifestyle Line of Credit debt. This debt will demonstrate whether the liquidation of fixed assets is sufficient in filling future deficiencies. Also, due to the fact that RazorPlan charges an annual interest rate on the balance of the Lifestyle Line of Credit, this also gives us insight as to whether a reverse mortgage solution could potentially work.

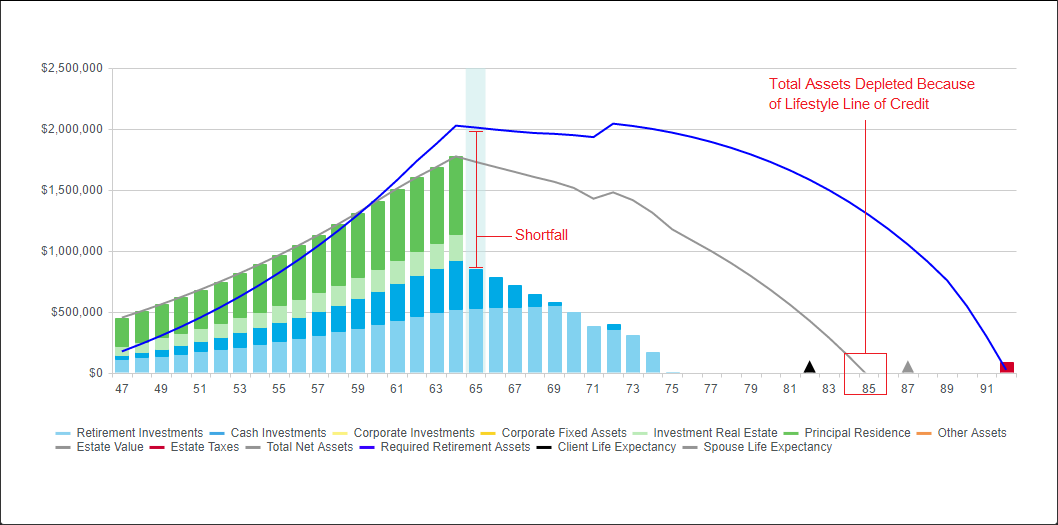

Below is an example of the Financial Assets Chart when liquidating fixed assets is not an adequate solution. We can see that because the Total Net Assets line is reduced to zero prior to age 92, the inclusion of Lifestyle Line of Credit has depleted the client’s net worth to zero. Even if the client liquidated all of their fixed assets, they still do not have enough to fund their lifestyle to age 92.

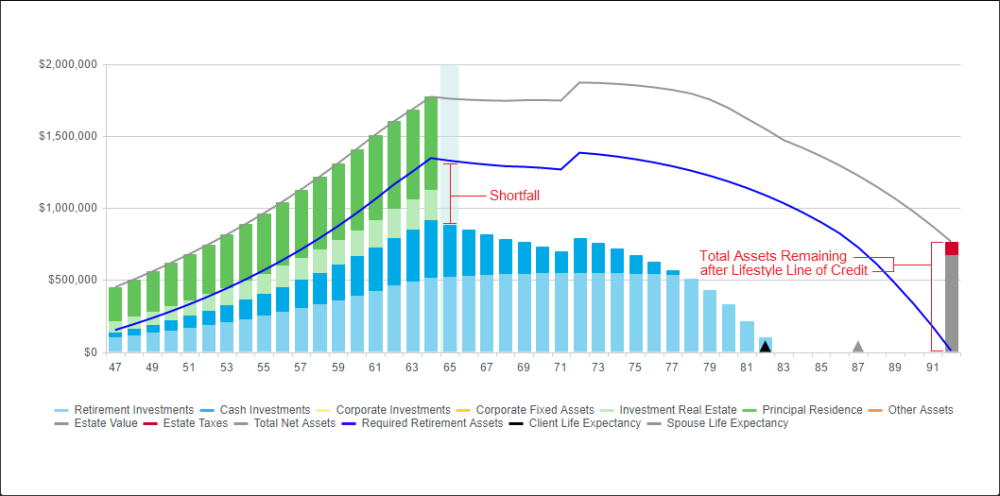

Below is an example of the Financial Assets Chart when liquidating fixed assets is an adequate solution. We can see that the Total Net Assets line is well above zero at age 92, even after the inclusion of Lifestyle Line of Credit. This indicates that the client could borrow or liquidate fixed assets to fill future lifestyle deficiencies.

Need more help with this?

Contact Razor Support