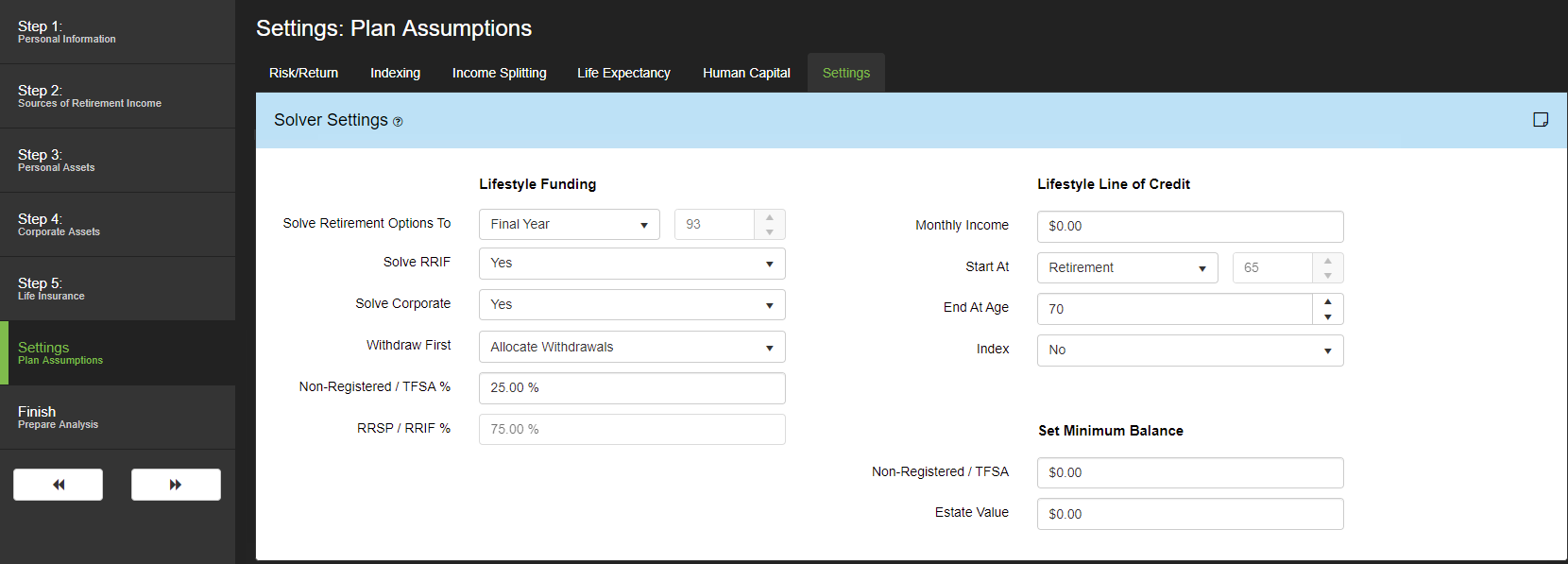

Solver Settings control how the software will solve for the retirement goals, provides the ability to model tax free income and lets users set minimum balances for certain assets areas.

Lifestyle Funding

Solve Retirement Options To: This setting allows you to choose which year you want the Retirement Options area to be solved for. Use the dropdown to select the Age setting which allows you to choose an age that is different from the Final Year of the plan. The four solves displayed in retirement options will then display the result to make retirement assets last until the selected age.

Solve RRIF: This field allows you to give the software the ability to automatically draw on RRIF assets to fill deficiencies in retirement. If set to ‘No’, the software will be limited to drawing minimum amounts only, even if deficiencies exist. If set to ‘Yes’, the software will be able to draw on these assets over the minimum when needed.

Solve Corporate: This field allows you to give the software the ability to draw on Corporate Investment & Securities in retirement. If ‘Yes’ is selected, the software will automatically create a dividend to utilize RDTOH (Refundable Dividend Tax on Hand) each year, beginning with the first year of retirement. The software will also utilize principal amounts to generate dividends to offset deficiencies in retirement when required. If ‘No’ is selected, the software will treat all Corporate Investment & Securities as fixed assets and will not be able draw down these assets to fund deficiencies in retirement.

Withdraw First: This field allows you to select the withdrawal order the program uses when making withdrawals to meet the desired retirement lifestyle. There are 3 options available in this field:

- Non-Registered / TFSA – If Non-Registered / TFSA is selected, RazorPlan will withdraw from the Non-Registered or TFSA accounts prior to the RRSP / RRIF accounts when there are lifestyle deficiencies.

- RRSP / RRIF – If RRSP / RRIF is selected, RazorPlan will meet lifestyle deficiencies with RRSP / RRIF withdrawals before making withdrawals from either the Non-registered or TFSA accounts. The RRSP / RRIF option is a way of modeling a RRIF meltdown.

- Allocate Withdrawals – The Allocate Withdrawals option displays the Non-Registered / TFSA % and RRSP / RRIF % fields where an withdrawal allocation can be set.

Non-Registered / TFSA %: This field sets the percentage of withdrawals from Non-Registered and TFSA accounts needed to fund lifestyle deficiencies. This field and the RRSP / RRIF % field need to add up to 100 %.

RRSP / RRIF %: This field sets the percentage of withdrawals from RRSP / RRIF accounts needed to fund lifestyle deficiencies. This field and the Non-Registered / TFSA % field need to add up to 100 %.

Lifestyle Line of Credit

Monthly Income: This field allows you to specify static Lifestyle Line of Credit amounts to draw each month for a specific period of time. This allows you to demonstrate the ability to borrow against fixed assets for discussion purposes.

Start At: Select ‘Retirement’ from the drop-down to have the monthly LOC income begin at retirement, or select ‘Age’ to establish a specific age.

End At Age: Enter the age to which you anticipate this monthly LOC income will continue as a numeric value. The stream of income will stop at that age.

Index: To specify whether monthly LOC income will grow with inflation, select ‘Yes’ or ‘No’ from the dropdown.

Set Minimum Balance

The following minimum balance data entry fields are only available in RazorPlan Advanced. You can upgrade to RazorPlan Advanced using the Billing tab in Your Account. If you have any questions, please contact support.

Non-Registered / TFSA: Enter the total value of the Non-Registered and TFSA assets that, at a minimum, will always be part of the client’s net worth. This minimum amount can be less than, equal to or even greater than the current balances of the Non-Registered and TFSA accounts. Setting a minimum value for Non-Registered and TFSA assets will impact the client’s cash flow and their attainable retirement income.

Estate Value: Enter a value that the clients would like their estate value to equal, at a minimum at the end of the planning period. This minimum amount will impact the client’s attainable retirement income that is displayed in Retirement Needs Option 1.

Need more help with this?

Contact Razor Support