The Corporate Estate Ledger displays the value of corporate assets on the death of the client and spouse / partner (if present). It outlines the flow of assets from the clients to the surviving heirs and the associated tax implications personally, corporately, and to the surviving heirs. An important consideration in these calculations is the method of corporate wind-up on death through proper Post-Mortem Planning. You can control how the corporate assets are wound up through the Share Value tab in Step 4 of Data Entry. Using the Post-Mortem Plan drop-down, you can select one of the four post-mortem planning options: Capital Gains, Double Taxation, Loss Carry-Back, and Pipeline Planning. Based on the selection made, the Corporate Estate Ledger will effectively demonstrate how this strategy will flow the corporate assets out to the surviving heirs.

This information is broken out into four different areas:

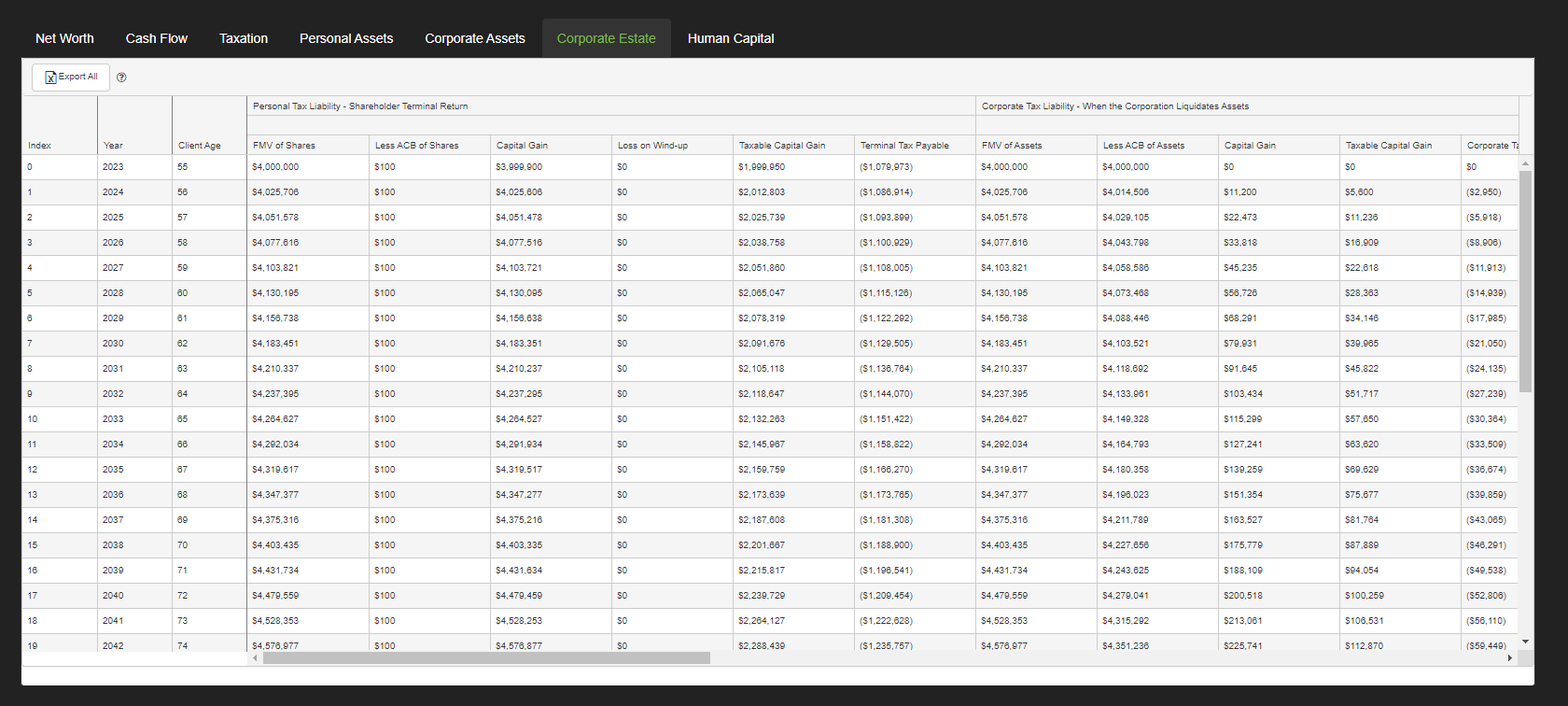

Personal Tax Liability

- FMV of Shares: The Fair Market Value of Shares column calculates the total Share Value Equity of all corporate assets including investments, real estate and goodwill.

- Less ACB of Shares: The Less Adjusted Cost Base (ACB) of Shares column calculates the total Cost Base of shares as entered through the Share Value tab in Step 4 of Data Entry.

- Capital Gain: This column calculates the capital gain created by the corporate assets by subtracting the Cost Base from the Fair Market Value of Assets.

- Loss on Wind-up: This column will only display a value when Loss Carry-Back is the post-mortem plan selected. This result is dependent on other corporate data and could trigger alternative minimum tax. The underlying math calculations are complex but typically this amount will offset the Capital Gain column.

- Taxable Capital Gain: This column calculates the taxable capital gain personally owed by subtracting any Loss on Wind-Up from the Capital Gain.

- Terminal Tax Payable: This columns show the tax payable by the shareholders on death, this amount is the tax payable on the Taxable Capital Gain column.

Corporate Tax Liability

- FMV of Assets: The Fair Market Value of Assets column calculates the total Share Value Equity of all corporate assets including investments, real estate and goodwill.

- Less ACB of Assets: The Less Adjusted Cost Base (ACB) of Assets column calculates the total Cost Base of the assets of the corporation. This amount is calculated based on the data entered in the various cost base fields (investments, real estate and goodwill) in Step 4 of data entry.

- Capital Gain: This column calculates the capital gain owed on corporate assets by subtracting the Cost Base from the Fair Market Value of Shares.

- Taxable Capital Gain: This column determines how much of the capital gain is taxable by applying the capital gain inclusion rate.

- Corporate Tax Payable: This column calculates the tax liability of the corporation itself based on the liquidation of corporate assets. It is calculated by applying the Top Corporate Tax Rate on Investment Income for the province of residence to the Taxable Capital Gain column.

Dividend Tax Liability

- ATV of Assets: This column displays the after-tax value (ATV) of all assets entered under the Corporate Assets data entry section.

- Death Benefit: The Death Benefit column displays the death benefit value of any corporately owned life insurance policies.

- RDTOH Refund: This column displays the tax refund created from the Refundable Tax on Hand (RDTOH) account when the cash is distributed to the heirs.

- Total Distribution: This column sums up the values from the ATV of Assets, Death Benefit and RDTOH Refund. This amount represents how much is being distributed to the heirs of the clients.

- Tax-Free Capital: This column displays the portion of the total distribution that is tax-free. This amount is calculated as the remainder of the total distributions after the Tax-free CDA and Taxable Dividend amounts are removed.

- Tax-Free CDA: This column displays the amount of the Capital Dividend Account (CDA) that is paid when cash is distributed to the heirs of the business owner. This amount is calculated based on the values entered for corporate owned life insurance, the starting / current CDA value, and the cost base of the corporation’s assets.

- Taxable Dividend: This column calculates the taxable dividends that results from adjusting the total distribution that is being paid out to the shareholders from the corporation. The taxable dividend is calculated as the Total Distribution less Tax-Free Capital and Tax-Free CDA amounts.

- Dividend Tax Payable: This column shows the tax payable on the Taxable Dividend created when the cash is distributed to the heirs of the corporation.

Total Corporate Tax Liability

- Personal Capital Gain: A summary column that displays the tax liability from the personal capital gain on the distribution of the corporate assets. The calculation of this column is shown in the Personal Tax Liability section of this ledger page.

- Corporate Capital Gain: A summary column that displays the tax liability from the capital gains at the corporate level. The calculation of this column is shown in the Corporate Tax Liability section of this ledger page.

- RDTOH Refund: This columns shows the refund created from the Refundable Tax On Hand (RDTOH) account when the dividend is paid.

- Personal Dividend: A summary column that displays the tax liability from the dividend distributed. The amount shown in this column is calculated in the Dividend Tax Liability section of this ledger page.

- Total Tax Liability: This column displays the sum of the amounts from the Personal Capital Gain column, the Corporate Capital Gain column, and the Personal Dividend column less the amount in the RDTOH Refund column.

- Potential Tax Rate: This columns is calculated by dividing the Total Tax Liability by the amount shown in the FMV of Shares column for the corporation.

- ATV to Heirs: This column shows the difference between the FMV of Shares and the Total Tax Liability. This is the After Tax Value (ATV) to the heirs of the shareholders.

- Percentage to Heirs: This column shows the ATV to Heirs column as a percentage of FMV of Shares, it is calculated as 1 minus the Potential Tax Rate column.

- Un-Used RDTOH: This column will display any RDTOH that is not being used in the calculation of the corporate estate for the shareholders.

- Un-Used CDA: This column will display any CDA that is not being used in the calculation of the corporate estate for the shareholders.

Need more help with this?

Contact Razor Support