The Risk Management tab provides charts that identify the need for life insurance. RazorPlan users will have access to a Human Capital Summary chart while RazorPlan Advanced users will have access to 4 additional charts, as outlined below. A drop down window is provided for accessing the additional charts that are available. The options provided in the drop down are Client First Death, Client Second Death, Spouse First Death and Spouse Second Death.

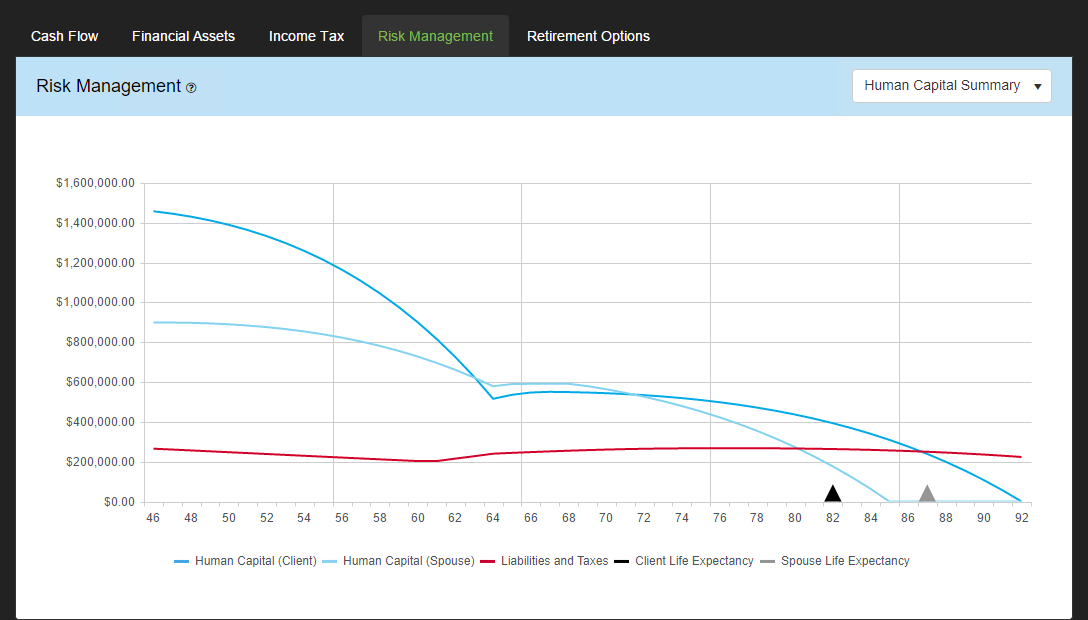

Human Capital Summary

Selecting Human Capital Summary outlines a client’s changing Human Capital value over the life of the analysis. This is the default option and the only view available to RazorPlan users. This chart helps to demonstrate how a client’s insurance needs will change over time. Vertical lines have been included to draw attention to the Human Capital value every 10 years. This can be useful when recommending a layered insurance solution.

- Human Capital Client – This represents the changing Human Capital value for the Client.

- Human Capital Spouse – This represents the changing Human Capital value for the Spouse/Partner.

- Liabilities and Taxes – This is equal to the estimated liabilities (Tax, Debt and Lifestyle Line of Credit) assuming second death at every age.

- Client Life Expectancy – The client’s assumed life expectancy that has been entered.

- Spouse Life Expectancy – The spouse’s assumed life expectancy that has been entered.

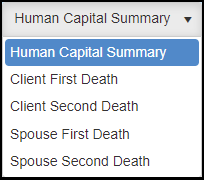

Client / Spouse First Death

When either of the first death options are selected this chart displays the impact the death of the selected person will have. So Client First Death shows the personal insurance needs in the event of the client dying before the Spouse and vice versa for Spouse First Death. In addition to showing the need for insurance this chart also displays any insurance benefits that will be paid at the selected person’s death.

- *Death Benefit – These bars represent any life insurance proceeds that would be received as a result of the selected person’s death. The amount displayed includes both the cash values (if any) and death benefits of all insurance policies entered for the selected person. All joint last to die policies are excluded on this chart.

- *Human Capital – This line represents the changing Human Capital value for the selected person.

- *Personal & Corporate Mortgage Debt – This line shows the total value of all outstanding personal and corporate debts. The balance outstanding on all real estate mortgages, credit cards, lines of credit and other loans entered on the Other Assets are included in this line. Plus any corporate real estate mortgage balances are also a part of this line.

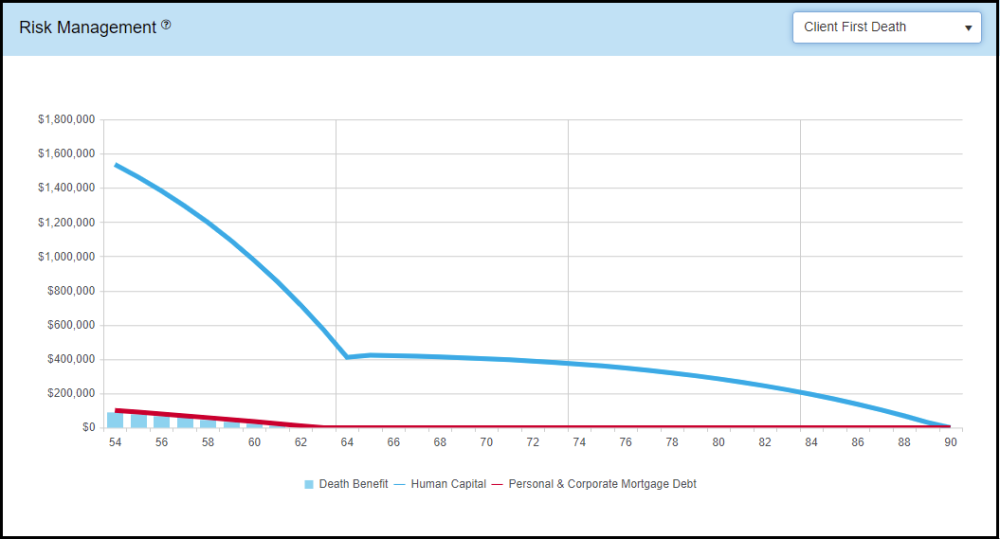

Client / Spouse Second Death

When either of the second death options are selected this chart displays the estate’s need for insurance. The second death charts show the debts and taxes that are payable assuming one of the clients has predeceased the selected person.

- *Death Benefit – These bars represent any life insurance proceeds that would be received as a result of the selected person’s death occurring second. The amount displayed includes both the cash values (if any) and death benefits of all insurance policies entered for the selected person plus any joint last to die policies.

- *Lifestyle Debt & Estate Taxes – This line has two components; Lifestyle Debt, which is the sum from any cash flow deficiencies; and Estate Taxes, which is the sum of the Personal Estate Taxes and Corporate Deferred Taxes from the Net Worth Ledger.

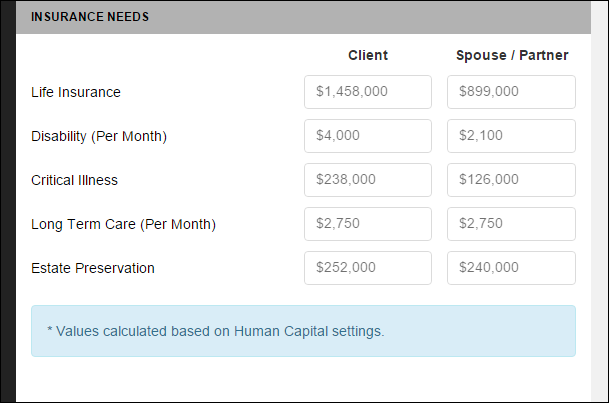

Insurance Needs Summary

The Risk Management Chart includes an Insurance Needs Summary as part of the Data Panel. This summary is only visible when viewing the Risk Management Chart.

This summary outlines the risk management and estate preservation needs at life expectancy. These values are controlled through the Human Capital Settings area of Data Entry. You can set the user defaults for any of these values through the Assumptions area of Your Account.

Life Insurance – This is typically set to Life Expectancy Human Capital but can be adjusted to represent a shorter time frame. For example, if you wish to only insure a 10 year period beyond the client’s death, you would select “10 Year Human Capital” from the Human Capital Settings area of Data Entry.

Disability Insurance – Typically, this is calculated as 60-70% of Retirement Human Capital divided by the number of months remaining to retirement. You can choose to adjust both the percent of income covered as well as the time frame for Human Capital. This approach is used to calculate a monthly human capital value required for long term disability and is similar to a traditional disability needs calculation. Both of these values can be adjusted through the Human Capital Settings area of Data Entry.

Critical Illness Insurance – Without sufficient information to go on, Critical Illness Needs can be tricky to calculate. The amount of insurance required will be based largely on the client’s age, marital status, health, income, etc. In addition, without knowing the illness suffered and its severity, it is nearly impossible to determine the appropriate amount of coverage. Because of this, RazorPlan allows you to choose any of the Human Capital values to use as Critical Illness need. Typically, this value is set as “3 Years Human Capital”. This represents the need to replace 3 years income should your client suffer a critical illness. This approach helps to establish a value for the clients in the event of a critical illness and allows you to move to the next level of discussion. You can set the Human Capital value through the Human Capital Settings area of Data Entry.

Long Term Care Insurance – There is no detailed LTC needs calculation within RazorPlan, the software calculates a flat value based on the client’s Retirement Lifestyle 1. This calculation is done as a percentage of Retirement Lifestyle 1 for 10 years. You can establish the percentage through the Human Capital Settings area of Data Entry.

Estate Preservation – This is equal to the estimated liabilities (Tax and Debt) at life expectancy. Should your client wish to pass the value of their estate on to their children, the Estate Preservation area outlines the Tax and Debt triggered on death that could deplete the estate to the heirs. This amount only includes Taxes, Debt, and Lifestyle Line of Credit. Other expenses, such as probate, are not included.

Need more help with this?

Contact Razor Support