The concept of a Lifestyle Line of Credit (LOC) was included in RazorPlan to help further the discussion when your clients fall short of funding their Retirement Income Needs. When a client falls short of funding their goals, the Lifestyle LOC is introduced and the software begins to borrow to fund deficiencies. The software tracks the value of this debt, charges an interest rate, and never makes a payment.

The value of the Lifestyle LOC will then offset the client’s Net Worth and help you determine whether sufficient fixed assets are available to offset the client’s deficiencies and whether a leverage or reverse mortgage strategy will work.

This concept is best examined through the use of a few examples. The below examples use the Cash Flow Chart and the Financial Assets Chart.

Example #1

Bill and Mary do not have sufficient Total Assets to fund their goals.

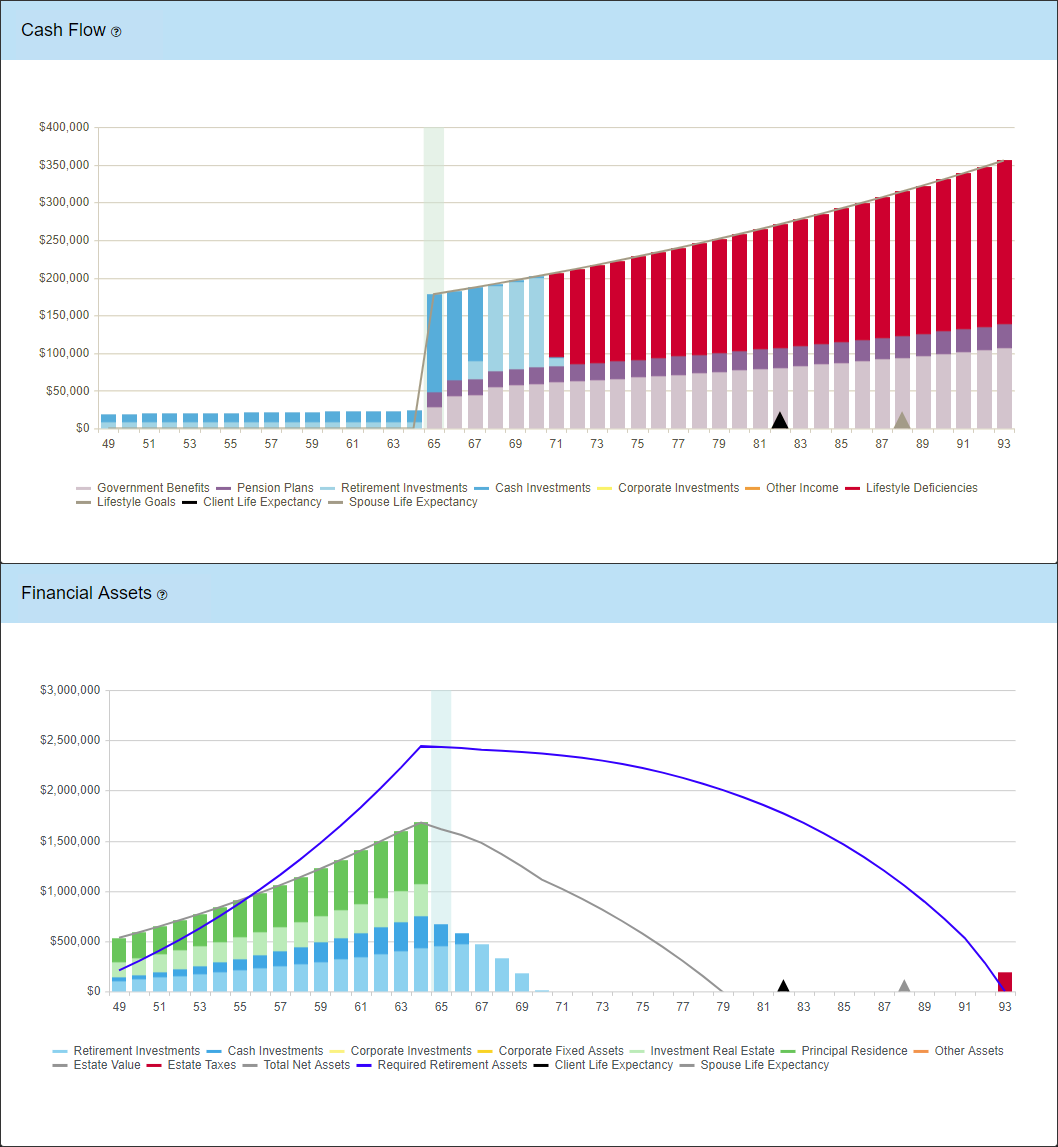

As we can see from the above Cash Flow Chart, Bill and Mary were unable to fund their lifestyle goals beyond age 70. At that time, the software began drawing money from the Lifestyle LOC to help fill the deficiencies. In the Financial Assets Chart we can see that the value of the Lifestyle LOC has completely depleted their Net Worth by age 79 and reduced the grey Net Worth line to $0. This tells us that a leverage strategy will not work as there are insufficient fixed assets to support it. Additionally, liquidation is insufficient as the blue Required Retirement Assets line is well over the total value of assets at retirement.

Example #2

Bill and Mary do not have sufficient Liquid Assets, and do not have sufficient Total Assets unless the principal residence is liquidated.

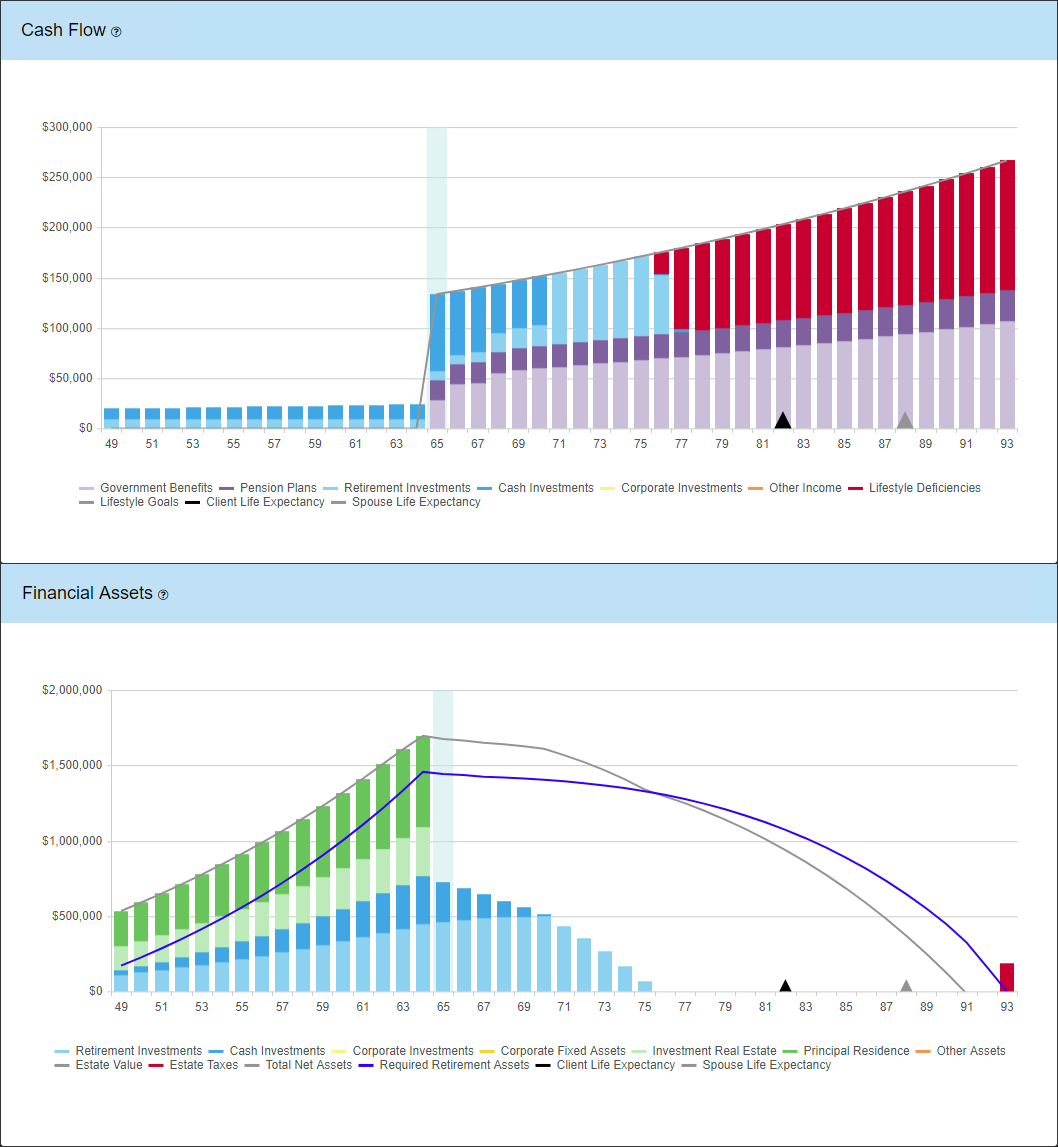

As we can see from the above Cash Flow Chart, Bill and Mary were unable to fund their lifestyle goals beyond age 75. At that time, the software began drawing money from the Lifestyle LOC to help fill the deficiencies. In the Financial Assets Chart we can see that a liquidation strategy may be sufficient in funding their shortfalls, but they would need to liquidate most of their fixed assets at retirement as seen by the blue Required Retirement Assets line in comparison to the grey Net Worth line. A leverage strategy would not work due to the inclusion of interest. Because of the interest charged, the value of the Lifestyle LOC has completely depleted the grey Net Worth line to $0 by age 91. The clients will likely need to revisit their goals or increase their wealth.

Example #3

Bill and Mary do not have sufficient Liquid Assets, but do have sufficient Total Assets including recreational property.

As we can see from the above Cash Flow Chart, Bill and Mary were unable to fund their lifestyle goals beyond age 84. At that time, the software began drawing money from the Lifestyle LOC to help fill the deficiencies. In the Financial Assets chart we can see that although they had large deficiencies, the value of the Lifestyle LOC at life expectancy has not entirely depleted the value of the grey Net Worth line. In fact, they still have substantial net worth remaining and a liquidation strategy may be the solution. The value of the recreational property (light green bars in Financial Assets Chart) more than fill the gap between liquid assets and the blue Required Retirement Assets line. By selling this property at retirement and investing the proceeds, the clients could eliminate all deficiencies in retirement.

In addition to a liquidation strategy, we could also examine the ability to borrow against their real estate properties. Because the Lifestyle LOC includes an interest rate, and because no payments are made, we have effectively modeled a reverse mortgage strategy. Although the Lifestyle LOC debt isn’t specifically applied to a property, it does directly offset Net Worth. In the above example we can see that even after introducing the Lifestyle LOC, the clients still have close to $1,500,000 remaining at life expectancy, as represented by the grey Net Worth line. This tells us that a reverse mortgage strategy is a viable solution. Furthermore, they could theoretically delay borrowing until age 85 as they have sufficient liquid assets to fund their lifestyle until that time.

Need more help with this?

Contact Razor Support