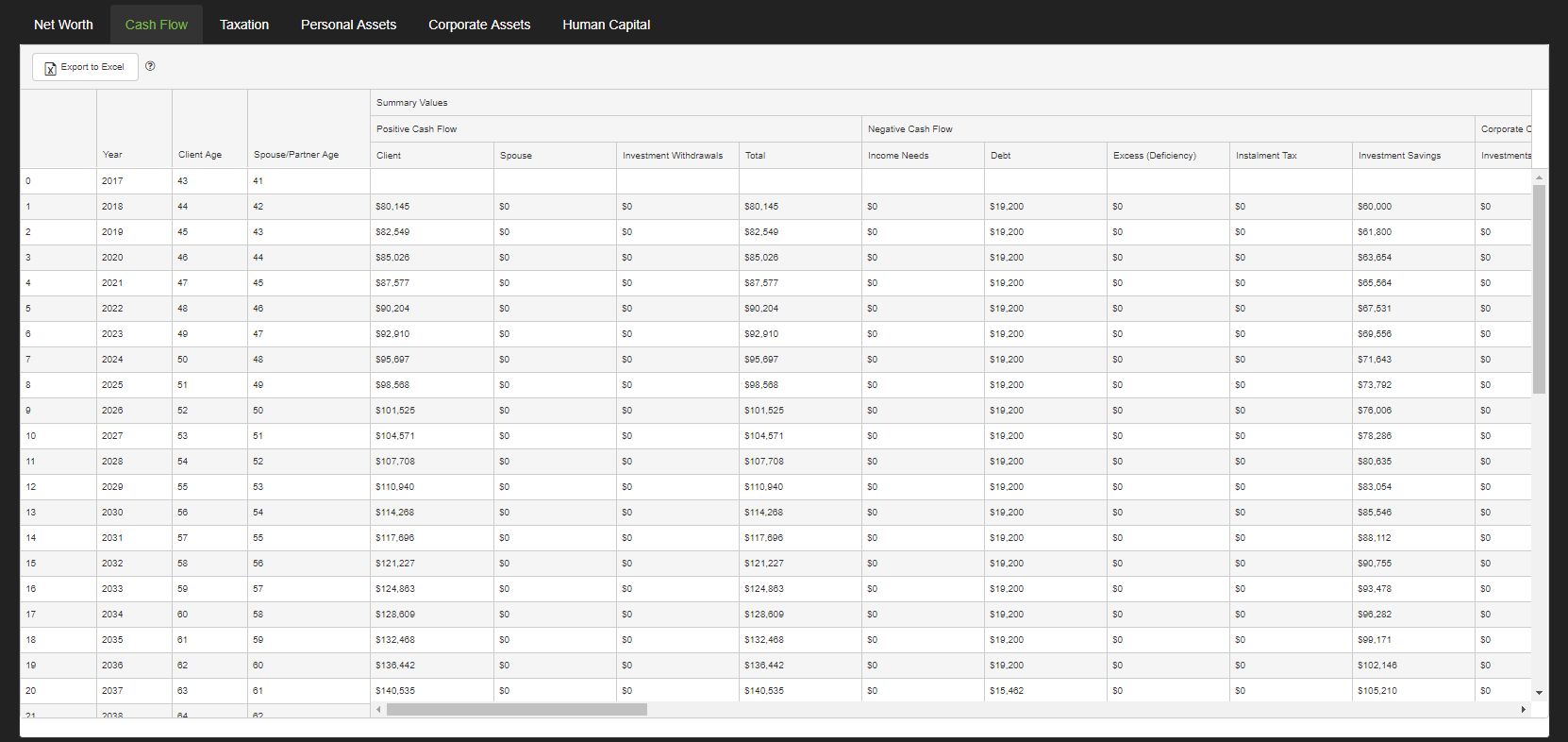

The Cash Flow Ledger outlines the income, savings and withdrawals of the clients. Income goals are compared to base income and investment withdrawals to determine if the clients have excesses or deficiencies in cash flow.

Positive Cash Flow

- Client – Total positive cash flow of the client. Includes after-tax employment earnings, CPP/QPP benefits, OAS benefits, pension plans and amounts entered in other income.

- Spouse/Partner – Total positive cash flow of the spouse/partner. Includes after-tax employment earnings, CPP/QPP benefits, OAS benefits, pension plans and amounts entered in other income.

- Investment Withdrawals – The sum of all investment withdrawals as outlined below.

- Loans – The sum of all income from loans, including draws against insurance policies.

- Tax Refund – Annual tax refunds that arise when the tax withheld is larger than the tax payable. (See Taxation ledger for more details).

- Total – Total positive cash flow for the client, spouse partner and from investment withdrawals.

Negative Cash Flow

- Installment Tax – This value is calculated as the tax payable less any taxes withheld at source for income from RRSPs, Pension Income, OAS benefits and Employment income. These values represent the additional tax that is payable that year.

- Income Needs – The annual after-tax Income Needs of the clients.

- Debt Payments – Total of annual payments being made against the mortgages and other debts.

- Insurance Premiums – Total annual premiums being paid on any personal insurance policies.

- Investment Savings – The annual total planned savings that are being made to all personal investment assets. (See investment savings below for the detailed categories).

- Excess (Deficiency) – Total positive cash flow less the sum of the installment tax, income needs, debt payments, insurance premiums and investment savings. This will determine the cash flow excesses (positive values) or deficiencies (negative values) for the year.

- Installment Tax – In the client’s retirement years this value is calculated as the tax payable less any taxes withheld at source for income from RRSPs, Pension Income, OAS benefits and Employment income. A negative value in this column represents a tax refund because more taxes were withheld than are payable in the year. Positive values represent the additional tax that is payable that year.

Tax Cash Flow

- Income Tax Payable – The annual total of the client and spouse/partner tax payable.

- Paid At Source – The total annual tax withheld at source. Withholding tax is calculated on employment income, income from retirement investments (above the minimums), pension plans and OAS.

- Paid By Excess – Difference between Income tax Payable and Paid At Source when there is excess (positive values) in the Excess (Deficiency) column.

- Net Tax Payable – When Paid At Source plus Paid by Excess less Income Tax Payable is negative there is a net tax payable. This amount becomes the installment tax in the following year.

- Net Tax Refund – When Paid At Source plus Paid by Excess less Income Tax Payable is positive there is a net tax refund. This amount becomes the tax refund in the following year.

Corporate Cash Flow

- Investment & Securities – The annual total planned savings that are being made to corporate investments and securities.

- Real Estate – Total annual payments being made against the mortgages on corporate real estate assets.

- Total – Sum of the Investment & Securities and the Real Estate corporate cash flows. This represents the annual cash flows of the corporate assets.

Base Income: Client and Spouse/Partner

- Employment Earnings – The annual income received from Employment Income. The amount shown in this column is net of withholding taxes.

- CPP/QPP Benefits – The annual income received from CPP/QPP.

- OAS Benefits – The annual payments received from Old Age Security.

- Pension Plans – The annual income received from Pension Plans. The amount shown in this column is net of withholding taxes.

- Dividends – Annual dividend income received (not grossed up) as entered on the Other Income tab of Step 1.

- Other Income – The annual income received from Working In Retirement.

- Total – The total of all base income including CPP/QPP Benefits, OASBenefits, Pension Plans, Employment Earnings and Other Income.

Investment Savings

- Retirement Plans – The combined total annual savings to RRSP/RRIF and Locked-In investments.

- Tax Savings – The total tax savings from deposits to RRSP/RRIF and Locked-In investments.

- Non-Registered – The combined total annual savings to Non-Registered investments. If ‘Auto Allocate’ in TFSA Data Entry set to ‘Yes’, some Non-Registered savings may be directed to TFSA savings automatically.

- TFSA – The combined total annual savings to TFSA investments.

- Total Savings – The sum of all above. This amount is also displayed in the negative cash flow section of this ledger page.

Debt & Insurance

- Principal Residence – The annual payments on the Principal Residence mortgage.

- Recreational Property – The annual payments on the Recreational Property mortgage.

- Investment Property – The annual payments on the Investment Property mortgage.

- Other Debts – The annual payment being made on Other Debts, including credit cards and personal lines of credit.

- Total Life Premiums – The annual premiums payable for personal life insurance policies.

- Total – The total annual cash flow directed toward mortgages. This amount is calculated as the sum of the Principal Residence, Recreational Property and Investment Property columns.

Investment Withdrawals

- LRIF/RRIF Minimum – The annual RRSP/RRIF and Locked-In Plan minimum withdrawals. Additional RRIF amounts needed to meet Retirement Income Needs over the minimums are displayed in the RRIF Top-Up column.

- Corporate (RDTOH) – The portion of any dividends paid from the corporate investments that will recoup the refundable dividend tax on hand. Additional dividends from the corporate investment accounts are displayed in the Corporate Top-Up column.

- Non-Registered – The total annual Non-Registered withdrawals needed to meet Retirement Income Needs.

- TFSA – The total annual TFSA needed to meet Retirement Income Needs.

- RRIF Top-Up – Additional annual RRIF needed to meet Retirement Income Needs.

- Corporate Top-Up – Annual dividends paid from Corporate Investments & Securities needed to meet Retirement Income Needs.

- Lifestyle LOC – Manually entered Monthly LOC entered through Data Entry. Although entered monthly, the annual equivalent is displayed.

- Total Withdrawal – The sum of all withdrawals needed to meet Retirement Income Needs.

Need more help with this?

Contact Razor Support