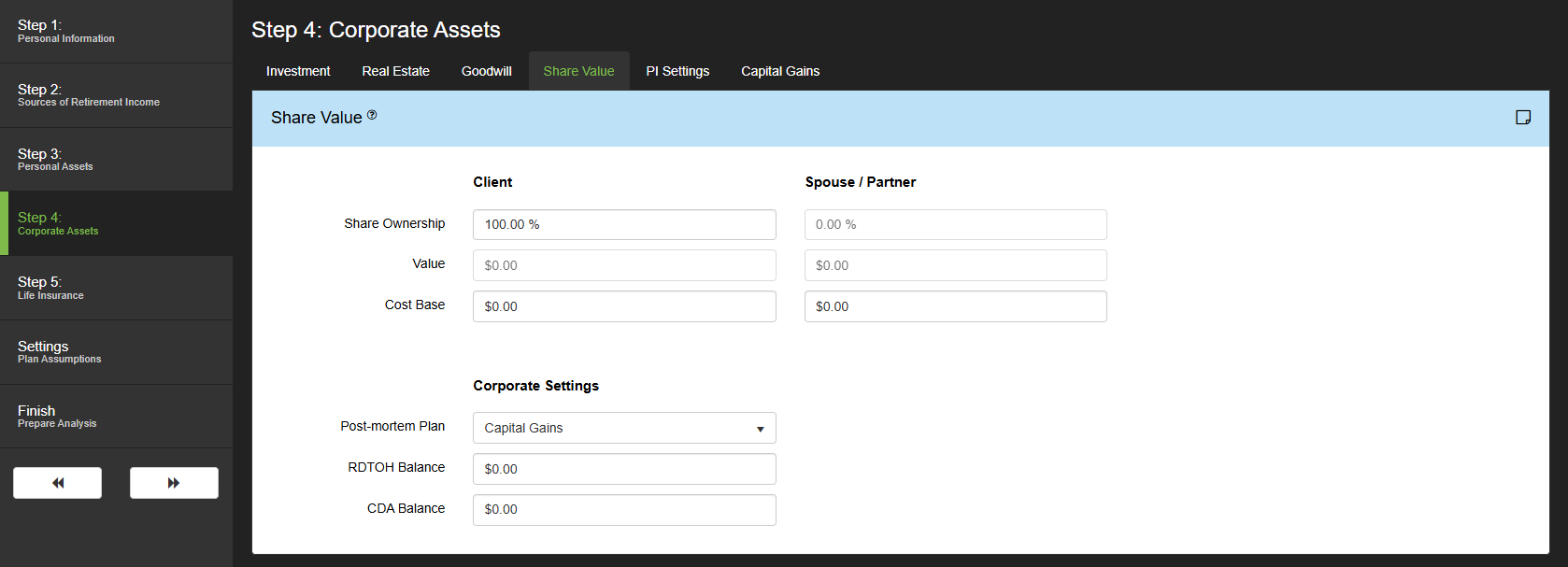

The value of corporate shares is automatically calculated as total corporate assets less total corporate liabilities. This area allows you to define Share Ownership and Cost Base.

Share Ownership: Enter the percentage of ownership in the Client’s name, Spouse/Partner will automatically update for the remaining balance.

Value: This field is automatically calculated based on the total value of all corporate assets (Investments & Securities, Real Estate, and Goodwill & Operations), less any remaining liabilities (Mortgage Amounts).

Cost base: Enter the Cost Base as it relates to the corporate shares ownership. The Cost Base is used to determine the cost of the shares for tax purposes. Increase the Cost Base to account for any Lifetime Capital Gains Exemption if the corporation is a qualifying small business corporation.

Post-mortem Plan: Select the method of post-mortem tax planning for the corporation. When the deemed disposition at death of the shares of the corporation are distributed, post mortem planning is utilized to minimize the overall tax burden. There are four post-mortem planning options to choose from in RazorPlan:

- Capital gains: Select this option to have RazorPlan calculate the taxes payable at death of the corporation’s shareholders as a capital gain for tax purposes. This option assumes no distribution to the estate in the form of a dividend.

- Double Taxation: Select this option to have RazorPlan calculate the wind-up of the corporation with a distribution to the estate in the form of a dividend. This method will determine the capital gain within the corporation and uses the RDTOH refund and CDA to determine the taxable dividend that can be distributed to the heirs.

- Loss Carryback: Select this option to have RazorPlan calculate the winding up of the corporation in a method that gives rise to a capital loss which is carried back to the shareholder’s terminal tax return to offset the capital gain at death.

- Pipeline Planning: Select this option to have RazorPlan calculate the taxes payable on the corporation using a pipeline strategy. This strategy impacts the ACB from the deemed disposition at death to avoid double taxation.

RDTOH Balance: Enter the current Refundable Tax On Hand (RDTOH) notional balance of the corporations. This amount is included as a refundable dividend in the calculations of corporate tax liability when estate planning.

CDA Balance: Enter the current Capital Dividend Account (CDA) notional balance of the corporations. This balance is added to any other calculated Capital Dividends and represented as a tax free dividend when determining the estate liability from the corporate assets.

Need more help with this?

Contact Razor Support