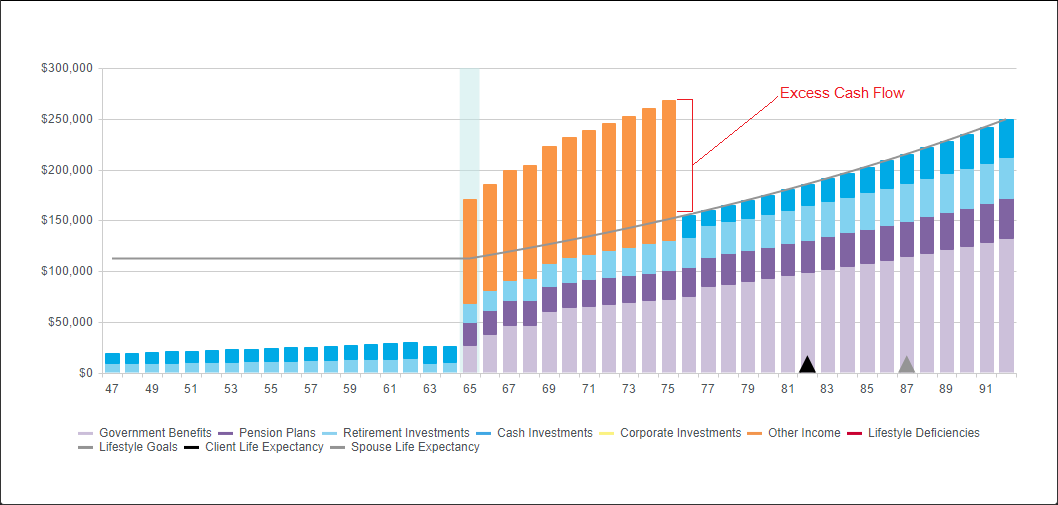

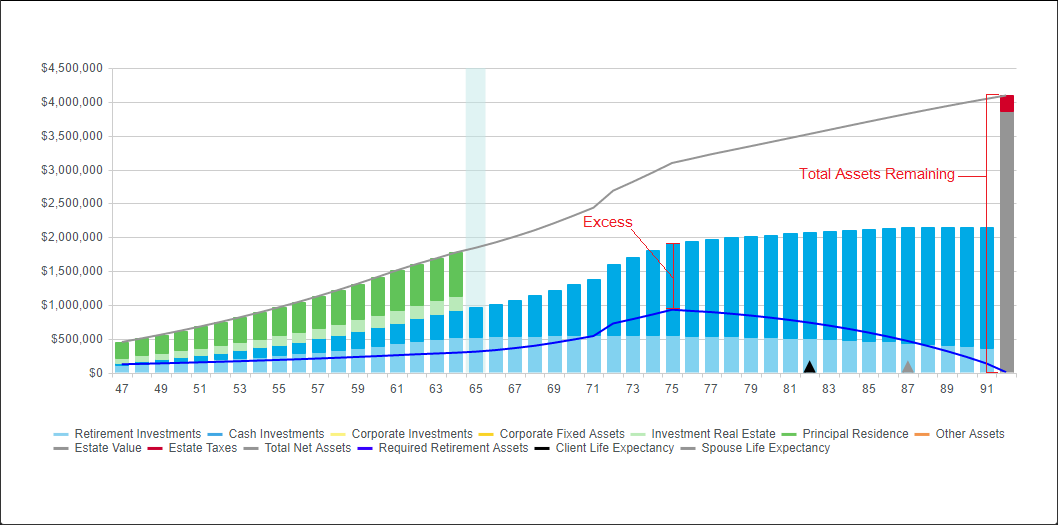

Below is an example of a situation where a client has more retirement income than necessary causing the software to deposit the excess. This deposit causes an increase in the value of liquid assets leaving a large net worth at life expectancy.

When a client has excess cash flow in retirement, you will see values over and above the client’s Retirement Income Needs. Typically, when a client has excess income in retirement the software will direct the excess towards the client’s investments automatically for use in future years. The software will deposit to the client’s Non-Registered Investments. If you have a client with an unrealistically low lifestyle goal in relation to their fixed income and assets, you may encounter very large excesses which will in turn create large assets at life expectancy.

The only time excess income in retirement will not be saved automatically is when the Spouse/Partner is working beyond the Client’s retirement age. For example, if the Client retires in 2025 and the Spouse retires 3 years later in 2028, the Spouse will continue working and earning Employment Income for those 3 years. Because the Spouse has not actually retired, the software will only use the Spouse’s Employment Income to help meet Retirement Income Needs, but will assume any excess Employment Income will be spent. In all other cases, the income will be saved.

Need more help with this?

Contact Razor Support