Portfolio construction

If an adviser is optimising a portfolio there are a range of constraints or rules they can insert into the portfolio model that will restrict the recommendations provided.

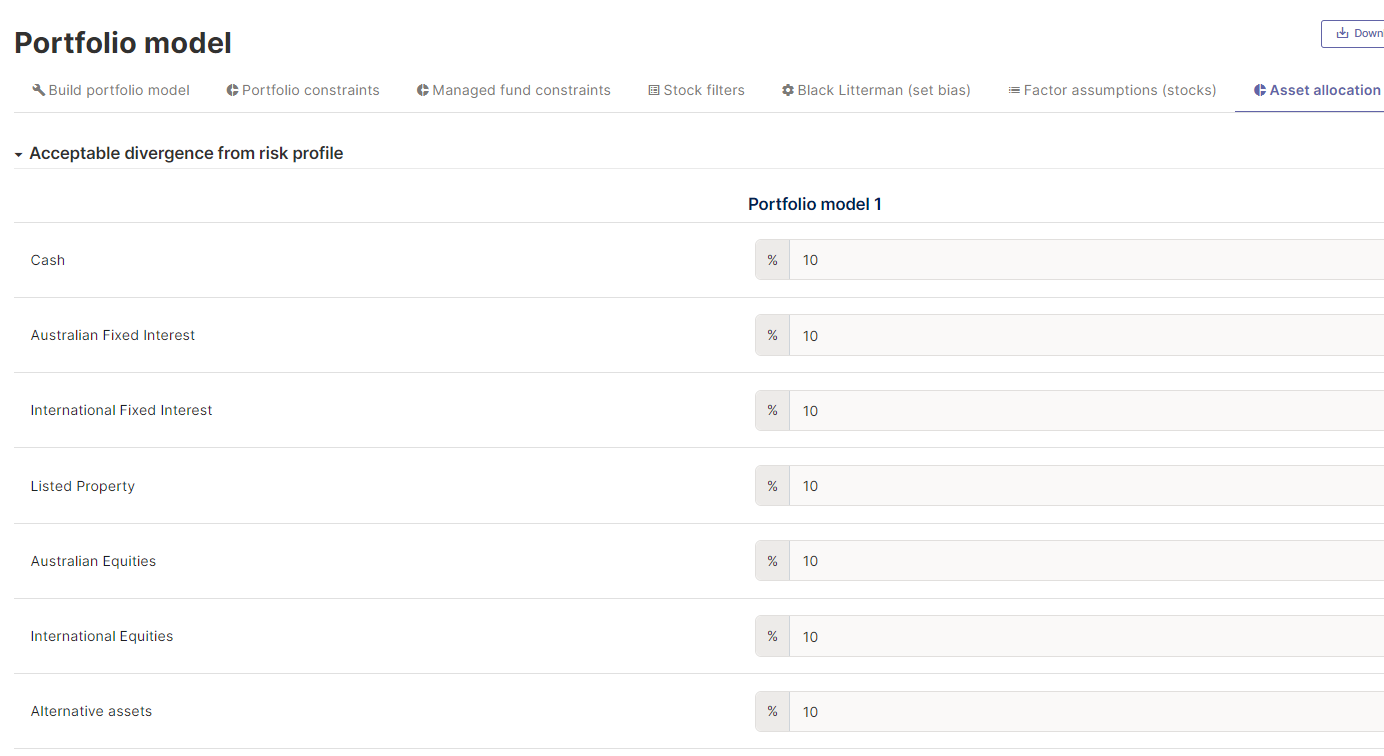

Risk profile

A client/s risk profile sets a constraint at an asset class level. Advisers can create some slack on the optimiser per asset class by creating a divergence from the target. For example, assume the target for cash is 15%. If the user selects an acceptable divergence of 15%, the optimiser can produce a portfolio with a cash allocation between 0-30%.

Constraints

The following constraints can be applied to the portfolio model:

| Constraint | Description |

|---|---|

| Minimum number of investments | This defines the bare minimum number of investments that the portfolio must incorporate. |

| Maximum direct stock exposure | This sets a maximum percentage of the portfolio allocation to direct equities |

| Maximum holding per asset | Sets a maximum position for each individual weighting |

| Maximum investment management fee | Sets a maximum acceptable fee for the total portfolio |

| Maximum transaction costs | Sets a maximum cost of implementing the model portfolio |

| *Maximum Capital Gains Tax | Sets a maximum capital gains tax that is acceptable for implementing the model portfolio. |

Post your comment on this topic.