A policyholder is anyone, who upon the occurrence of a contingency insured against, can claim upon a policy of insurance. A customer (client) is defined as a policyholder or a prospective policyholder who makes the arrangements preparatory to him/her concluding a contract of insurance.

Customers are either classed as consumers or commercial customers.

- Consumer – any natural person who is acting for purposes which are outside his/her trade or profession (sometimes called retail customers).

- Commercial Customer – a customer who is not a consumer

If it is not clear whether a customer is a consumer or commercial customer, then they must be treated as a consumer.

If a customer is acting in the capacity of both a consumer and a commercial customer in relation to a particular contract of insurance, the customer is a commercial customer e.g., a Sole Trader taking out a commercial vehicle policy – they are deemed a commercial customer.

However, if the customer enters into a contract of insurance mainly for purposes unrelated to their trade or profession then for the purposes of customers disclosure obligations and claims handling, they must be treated as a consumer.

You need to establish the customer type – Consumer or Commercial – as it affects various aspects of the sales process including:

- Customer’s disclosure obligations

- Required Product documentation – IPID or Policy Summary

- Commission disclosure

- Cooling–off rights

- Renewal Invitations content

Examples of customer classification include:

A taxi driver (operating as a sole trader) buys motor insurance policy for a car which will only be used in his business as a taxi driver. The taxi driver will be a commercial customer.

A taxi driver buys motor insurance for a car for his use (as a sole trader taxi driver) and for his wife to use for taking the children to school. The taxi driver is classed as a commercial customer.

An individual taking out a motor policy for social, domestic and pleasure use only will be classed as a consumer.

A company that takes out private medical insurance for its employees would be classed as a commercial sale, but the individual employees are classed as ‘consumer beneficiaries’ and when they claim or complain, they should be treated as a consumer.

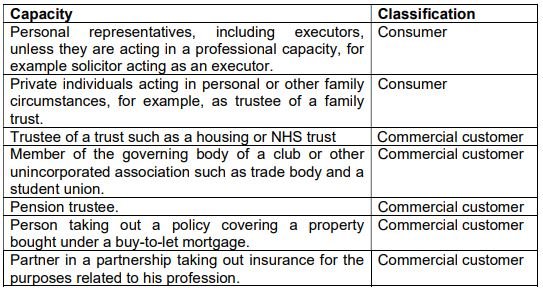

Private individuals however can act in a number of capacities. The FCA has provided guidance on how individuals may be categorised in the table below.

Post your comment on this topic.